Backtrader 文档学习-Indicators混合时间周期

1.不同时间周期

如果数据源在Cerebro引擎中具有不同的时间范围和不同的长度,指示器将会终止。

比如:data0是日线,data1是月线 。

pivotpoint = btind.PivotPoint(self.data1)

sellsignal = self.data0.close < pivotpoint.s1

当收盘低于s1线(第一支撑位)时为卖出信号

PivotPoint可以在更大的时间范围内工作

在以前的版本报错:

return self.array[self.idx + ago]

IndexError: array index out of range

原因是:self.data.close提供第一个bar的值,但PivotPoint(以及s1行)只有在一个完整月过去后才会有值,相当于self.data0.close的22个值。在这22个close值,s1的Line还没有值,从底层数组获取它的尝试失败,报错超出范围。

Line对象支持(ago)运算符(Python中的__call__特殊方法)来传递自身的延迟版本:

close1 = self.data.close(-1)

In this example the object close1 (when accessed via [0]) always contains the previous value (-1) delivered by close. The syntax has been reused to accomodate adapting timeframes. Let’s rewrite the above pivotpoint snippet:

对象close1(通过[0]访问时)始终包含close提供的前一个值(-1)。语法将重写以适应时间框架。重写上面的pivotpoint 片段:

pivotpoint = btind.PivotPoint(self.data1)

sellsignal = self.data0.close < pivotpoint.s1()

看看()是如何在没有参数的情况下执行的(在后台没有提供任何参数)。发生了以下情况:

- pivotpoint.s1()返回内部LinesCoupler对象,该对象遵循较大范围周期,coupler用来自实际s1的最新值填充,从默认值NaN开始 。

在后面章节中的参数说明:

PivotPoint Formula:

- pivot = (h + l + c) / 3 # variants duplicate close or add open

- support1 = 2.0 * pivot - high

- support2 = pivot - (high - low)

- resistance1 = 2.0 * pivot - low

- resistance2 = pivot + (high - low)

对应计算后的Line: - p

- s1

- s2

- r1

- r2

运行结果:

0069,0069,0014,2005-04-11,3080.60,3043.16,0.00

0070,0070,0014,2005-04-12,3065.18,3043.16,0.00

0071,0071,0014,2005-04-13,3080.54,3043.16,0.00

0072,0072,0014,2005-04-14,3075.33,3043.16,0.00

0073,0073,0014,2005-04-15,3013.89,3043.16,1.00

0074,0074,0015,2005-04-18,2947.79,2988.96,1.00

0075,0075,0015,2005-04-19,2957.37,2988.96,1.00

0076,0076,0015,2005-04-20,2944.33,2988.96,1.00

0077,0077,0015,2005-04-21,2950.34,2988.96,1.00

0078,0078,0015,2005-04-22,2976.39,2988.96,1.00

0079,0079,0016,2005-04-25,2987.05,2935.07,0.00

0080,0080,0016,2005-04-26,2983.22,2935.07,0.00

0081,0081,0016,2005-04-27,2942.62,2935.07,0.00

在长度为74 的时候,close < s1 。出现signal 。

2.代码

from __future__ import (absolute_import, division, print_function,

unicode_literals)

import argparse

import backtrader as bt

import backtrader.feeds as btfeeds

import backtrader.indicators as btind

import backtrader.utils.flushfile

class St(bt.Strategy):

params = dict(multi=True)

def __init__(self):

self.pp = pp = btind.PivotPoint(self.data1)

#print(dir(pp))

pp.plotinfo.plot = False # deactivate plotting

if self.p.multi:

pp1 = pp() # couple the entire indicators

self.sellsignal = self.data0.close < pp1.s1()

else:

self.sellsignal = self.data0.close < pp.s1()

def next(self):

txt = ' , '.join(

['%04d' % len(self),

'%04d' % len(self.data0),

'%04d' % len(self.data1),

self.data.datetime.date(0).isoformat(),

'%.2f' % self.data0.close[0],

'%.2f' % self.pp.s1[0],

'%.2f' % self.sellsignal[0]])

print(txt)

def runstrat():

args = parse_args()

cerebro = bt.Cerebro()

data = btfeeds.BacktraderCSVData(dataname=args.data)

cerebro.adddata(data)

cerebro.resampledata(data, timeframe=bt.TimeFrame.Weeks) # 增加周线

cerebro.resampledata(data, timeframe=bt.TimeFrame.Months) # 增加月线

cerebro.addstrategy(St, multi=args.multi)

cerebro.run(stdstats=False, runonce=False)

if args.plot:

cerebro.plot(style='bar')

def parse_args():

parser = argparse.ArgumentParser(

formatter_class=argparse.ArgumentDefaultsHelpFormatter,

description='Sample for pivot point and cross plotting')

parser.add_argument('--data', required=False,

default='./datas/2005-2006-day-001.txt',

help='Data to be read in')

parser.add_argument('--multi', required=False, action='store_true',

help='Couple all lines of the indicator')

parser.add_argument('--plot', required=False, action='store_true',

help=('Plot the result'))

return parser.parse_args()

if __name__ == '__main__':

runstrat()

允许参数说明:

python ./mixing-timeframes.py --help

usage: mixing-timeframes.py [-h] [--data DATA] [--multi] [--plot]

Sample for pivot point and cross plotting

optional arguments:

-h, --help show this help message and exit

--data DATA Data to be read in (default: ./datas/2005-2006-day-001.txt)

--multi Couple all lines of the indicator (default: False)

--plot Plot the result (default: False)

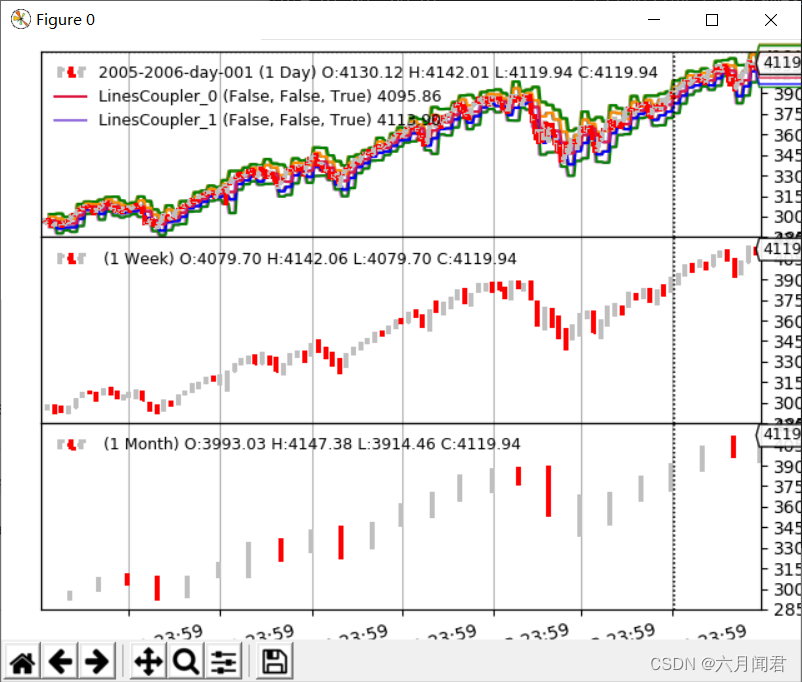

可以看到,日线、周线和月线,三个周期的数据,在cerebro 通过init中Indicator的初始化,在next中打印数据长度,数据和signal,执行结果:

3. 修改为不用args参数

在jupter中可以执行:

from __future__ import (absolute_import, division, print_function,

unicode_literals)

import backtrader as bt

import backtrader.feeds as btfeeds

import backtrader.indicators as btind

import backtrader.utils.flushfile

%matplotlib inline

class St(bt.Strategy):

params = dict(multi=True)

def __init__(self):

self.pp = pp = btind.PivotPoint(self.data1)

pp.plotinfo.plot = False # deactivate plotting

if self.p.multi:

pp1 = pp() # couple the entire indicators

self.sellsignal = self.data0.close < pp1.s1

else:

self.sellsignal = self.data0.close < pp.s1()

def next(self):

txt = ','.join(

['%04d' % len(self),

'%04d' % len(self.data0),

'%04d' % len(self.data1),

self.data.datetime.date(0).isoformat(),

'%.2f' % self.data0.close[0],

'%.2f' % self.pp.s1[0],

'%.2f' % self.sellsignal[0]])

#print(txt)

def runstrat(args_plot):

#cerebro = bt.Cerebro()

#data = btfeeds.BacktraderCSVData(dataname=args.data)

cerebro = bt.Cerebro()

stock_hfq_df = get_code('000858')

start_date = datetime.datetime(2020, 1, 1) # 回测开始时间

end_date = datetime.datetime(2020, 12, 31) # 回测结束时间

data = bt.feeds.PandasData(dataname=stock_hfq_df, fromdate=start_date, todate=end_date) # 加载数据

# Add the Data Feed to Cerebro

cerebro.adddata(data)

cerebro.resampledata(data, timeframe=bt.TimeFrame.Weeks)

cerebro.resampledata(data, timeframe=bt.TimeFrame.Months)

#cerebro.addstrategy(St, multi=args.multi)

cerebro.addstrategy(St, multi=True)

cerebro.run(stdstats=False, runonce=False)

if args_plot:

cerebro.plot(iplot=False,style='bar')

if __name__ == '__main__':

args_plot = True

runstrat(args_plot)

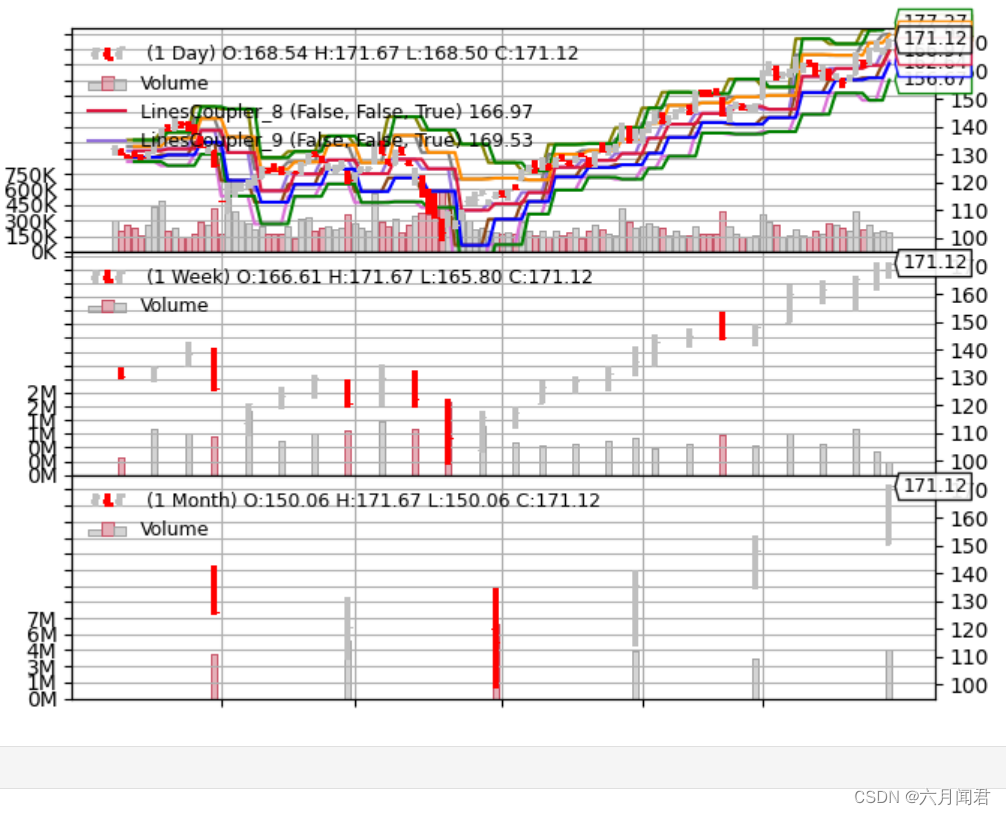

执行效果:

4.Indicator Reference

Indicator 参考说明,参数方法太多了,随用随学吧。